A stable financial system is essential for a well-functioning economy. It is characterised by the fact that its participants fulfil their respective functions smoothly and are able to withstand shocks. The SNB makes an important contribution to the stability of the financial system in Switzerland. It fulfils this mandate by, among other things, analysing sources of risk to the financial system and identifying areas where action is needed.

In its Financial Stability Report 2025, the SNB presents its latest assessment of the stability of the Swiss financial system.

Key points

- Economic and financial conditions relevant for the Swiss financial sector have deteriorated over the past 12 months. In particular, trade policy tensions sharply increased volatility in financial markets in spring 2025, weighed on global stock prices and caused corporate credit risk premia to climb.

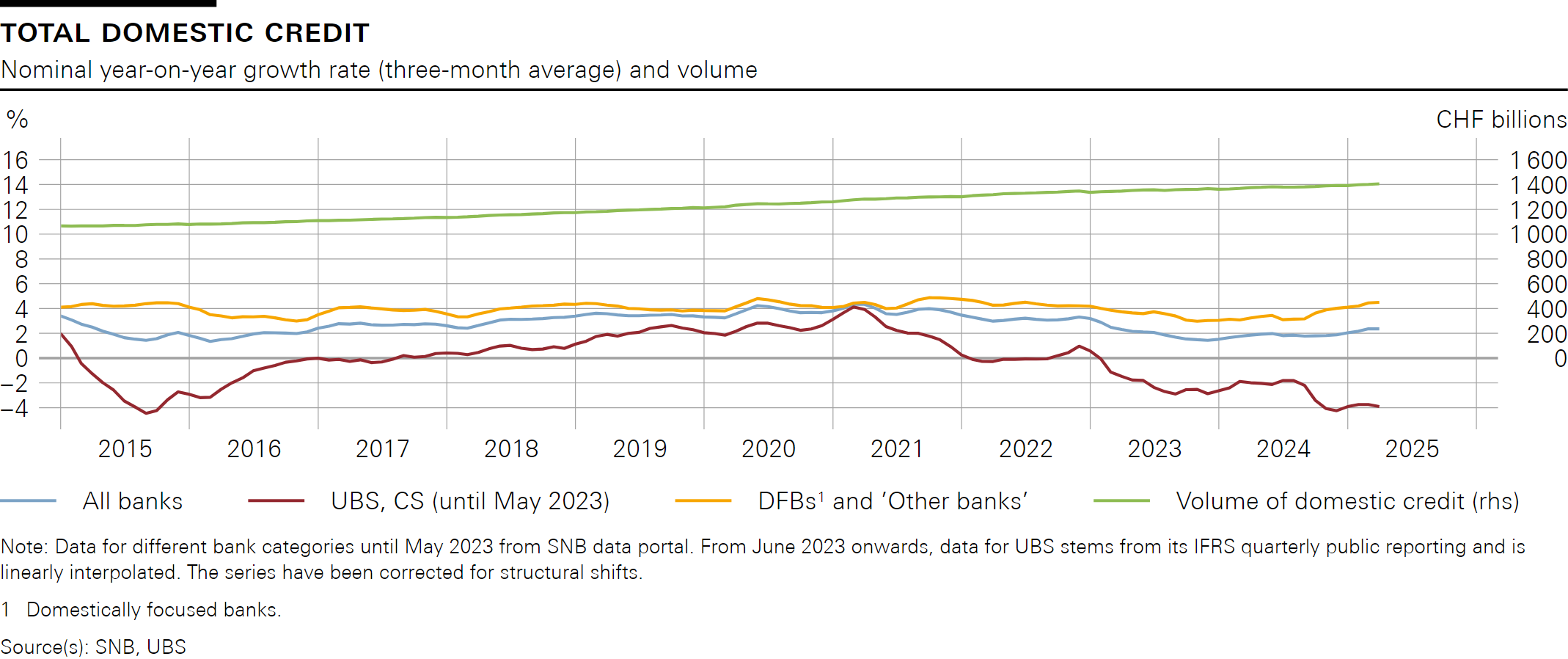

- In the Swiss credit market, outstanding loans have continued to increase despite structural changes in recent years. These include the acquisition of Credit Suisse by UBS and the introduction of the Basel III standards.

- For the Swiss banking sector as a whole, profitability improved in 2024, driven by UBS. Overall, banks’ capital buffers reflect significant loss-absorbing and lending capacity. In addition, banks hold substantial liquidity buffers.

- The interest rate environment weighed on domestically focused banks’ profitability, while their capital buffers remained stable. Thanks to their buffers, banks should be able to withstand adverse developments.

- For the three domestically focused systemically important banks (PostFinance, Raiffeisen Group, Zürcher Kantonalbank), profitability decreased. The capital ratios of Raiffeisen Group and Zürcher Kantonalbank are significantly above regulatory requirements. In comparison, PostFinance’s capital buffers are smaller.

- UBS’s operating profitability improved in 2024, but the costs of the integration of Credit Suisse continue to weigh on the bank’s profitability. UBS already meets the capital requirements applicable as of 2030.

- Banking regulation in Switzerland needs to be strengthened further in the aftermath of the crisis at Credit Suisse. The SNB supports the Federal Council’s efforts in this regard.

- Besides banks, non-bank financial intermediaries (NBFIs) also play a significant role in the domestic financial sector.

Banking regulation in Switzerland needs to be strengthened further

The crisis at Credit Suisse highlighted weaknesses in the existing regulatory framework for the banking sector. Decisive action must now be taken in order to further strengthen financial stability in Switzerland. As part of the reform of the ‘too big to fail’ (TBTF) regulations, the Federal Council has proposed a package of crisis prevention and crisis management measures to address these weaknesses. The SNB supports the Federal Council’s proposals. In the SNB’s view, the measures aimed at increasing the collateral prepared for obtaining liquidity support from central banks and strengthening capital requirements are particularly relevant.

Precautionary measures for liquidity risks

Experience from the 2022 - 2023 banking crisis in the US and in Switzerland highlighted the rapid pace at which liquidity outflows from banks can occur. When clients lose confidence in a bank, they withdraw their money quickly. This is accelerated by technological change. During the 2022 - 2023 banking crisis, liquidity buffers that were regarded as comfortable were thus rapidly depleted. Experience has shown that banks should prepare well for the risk of a rapid outflow of liquidity. In particular, they must prepare sufficient collateral that they can assign to the SNB and foreign central banks should they find themselves in need of liquidity support from central banks.

Strengthening capital requirements

The purpose of capital regulation for banks is to ensure that they can absorb even large losses in times of crisis without getting into financial distress. However, the crisis at Credit Suisse showed that reported capital ratios currently do not always adequately reflect a bank’s actual loss-absorbing capacity. The measures proposed by the Federal Council are aimed at addressing these weaknesses. In particular, the aim is to strengthen capital requirements for the parent bank within a banking group such as UBS. Specifically, the Federal Council proposes that the parent bank’s participations in foreign subsidiaries be fully deducted from Common Equity Tier 1 (CET1) capital, i.e. fully backed with capital. From a financial stability perspective, such a full deduction is the best solution.

«The right lessons have been learnt from the crisis at Credit Suisse. Banking regulation in Switzerland now needs to be strengthened in a targeted manner. The SNB supports the measures proposed to this end by the Federal Council as part of the ‘too big to fail’ regulations.»

Antoine Martin, Vice Chairman of the Governing Board, Swiss National Bank

Swiss credit market: volumes continue to grow

The Swiss credit market has been facing a number of changes in recent years. In 2022 and 2023, interest rates increased significantly again for the first time in 15 years. Furthermore, UBS acquired Credit Suisse and the Basel III standards came into force. Despite these major changes, credit volumes have continued to grow and, with the decline in interest rates in 2024, growth has even accelerated.

Structural shift in credit market due to UBS’s acquisition of Credit Suisse

The acquisition of Credit Suisse by UBS has changed the credit market landscape. Some of Credit Suisse’s former customers have entered into new credit relationships with other banks – for diversification purposes, for example. Accordingly, credit volumes in the rest of the banking sector have increased (cf. chart 1 under «downloads»). Banks’ capital and liquidity buffers have played a key role in helping them cope with this structural shift in the market.

Introduction of final Basel III standards

The final Basel III standards came into force in January 2025. Despite this fundamental reform, overall, no significant impact on the lending capacity of the Swiss banking sector is to be expected: The final Basel III standards were designed with the aim of leaving banks’ capital requirements unchanged overall. However, the reform does lead to more risk-sensitive capital requirements. While they increase for riskier segments such as building loans, they decrease for lower-risk segments such as owner-occupied properties. For domestically focused banks, which are typically active in mortgage lending in Switzerland, the new standards may result in lower capital requirements.

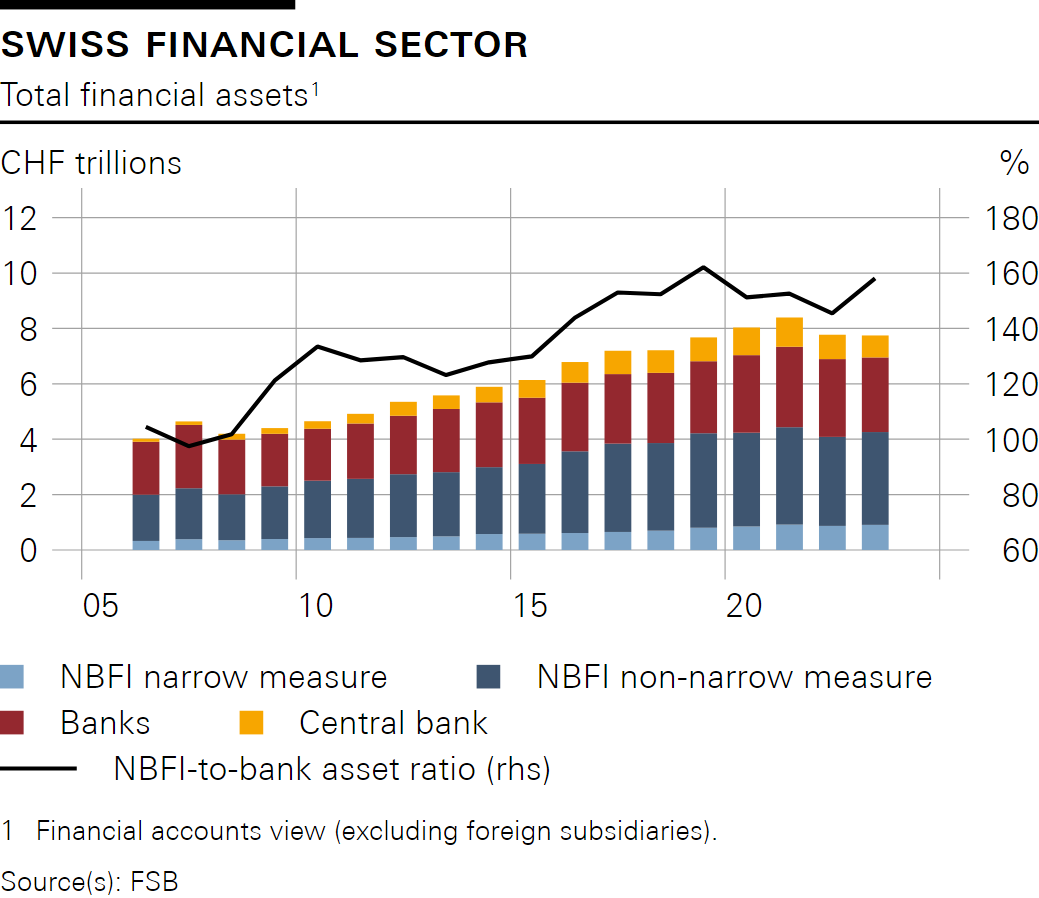

Non-bank financial intermediaries play significant role in financial sector

Besides banks, non-bank financial intermediaries (NBFIs) also play a significant role in the domestic financial sector. The Swiss NBFI sector is large and its growth has outpaced that of the banking sector since the global financial crisis (cf. chart 2 under «downloads»). The NBFI sector encompasses investment funds, pension funds, insurance companies, securities firms and other players.

The subset of Swiss NBFIs that are exposed to such bank-like vulnerabilities is relatively small. However, the extent of leverage and liquidity risk varies significantly across individual NBFIs. Moreover, interlinkages between Swiss banks and both domestic and foreign NBFIs are material. Going forward, more and better data is needed for assessing financial stability risks from NBFIs in Switzerland.

News conference of the SNB of 19 June 2025 - Introductory remarks by Antoine Martin, Vice Chairman of the Governing Board

Required category: Third-party

Please accept the relevant category to view this content.

{kind=link}

{kind=link}