Monetary policy assessment of 11 December 2025

Swiss National Bank leaves SNB policy rate unchanged at 0%

The Swiss National Bank is leaving the SNB policy rate unchanged at 0%. Banks' sight deposits held at the SNB will be remunerated at the SNB policy rate up to a certain threshold. The discount for sight deposits above this threshold still stands at 0.25 percentage points. The SNB remains willing to be active in the foreign exchange market as necessary.

Inflation in recent months has been slightly lower than expected. In the medium term, however, inflationary pressure is virtually unchanged compared to the last monetary policy assessment. The monetary policy helps to keep inflation within the range consistent with price stability and supports economic development. The SNB will continue to monitor the situation and adjust its monetary policy if necessary, in order to ensure price stability.

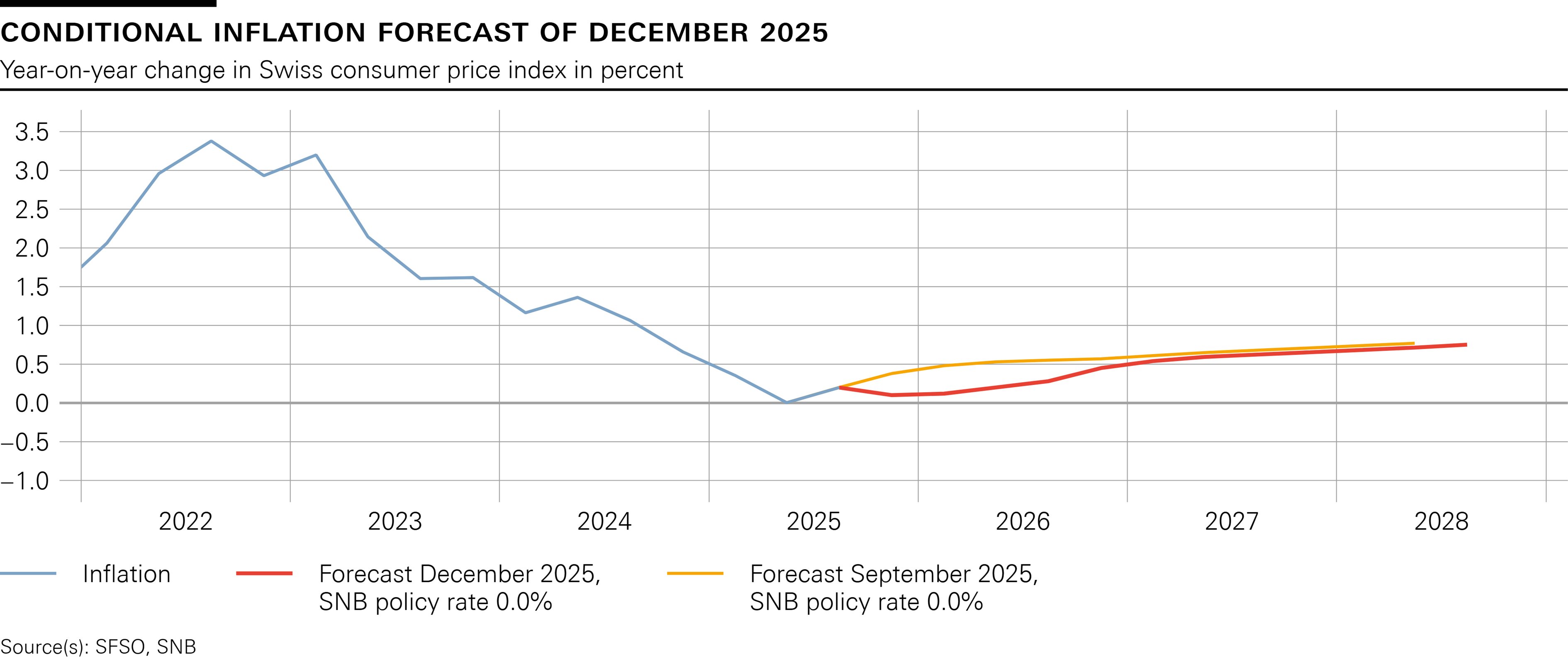

Inflation has declined slightly since the last monetary policy assessment. It decreased from 0.2% in August to 0.0% in November. Lower inflation in the hotel industry, as well as for rents and clothing, contributed in particular to this decline.

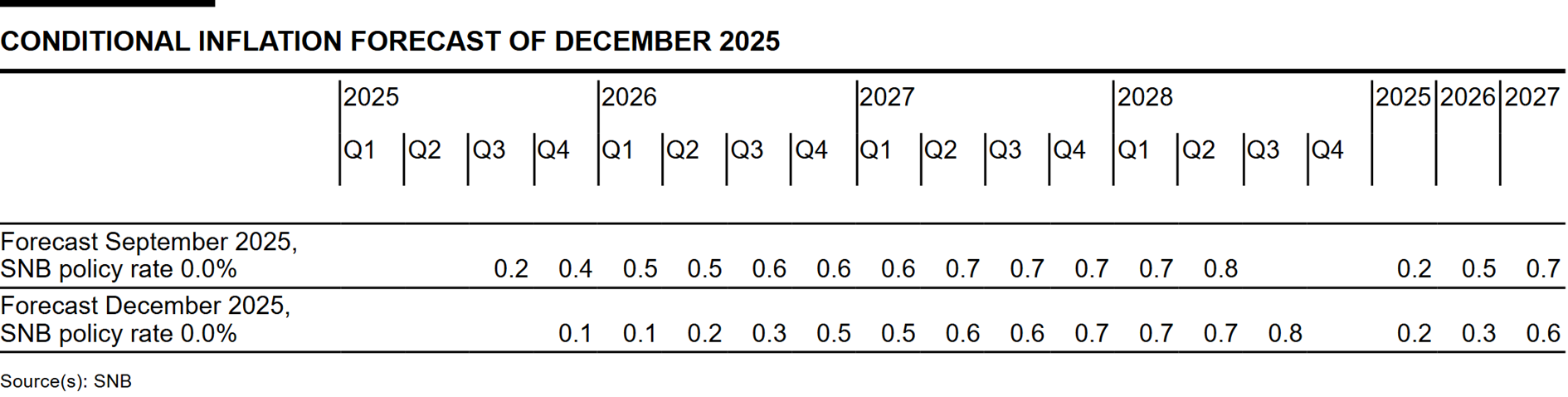

Inflationary pressure in the medium term is virtually unchanged compared to the previous quarter. Although the conditional inflation forecast is somewhat lower in the short term than in September, there is only little change in the medium term. The forecast is within the range of price stability over the entire forecast horizon (cf. chart). It puts average annual inflation at 0.2% for 2025, 0.3% for 2026 and 0.6% for 2027 (cf. table). The forecast is based on the assumption that the SNB policy rate is 0% over the entire forecast horizon.

Global economic growth was stronger than expected in the third quarter. Although US tariffs and trade policy uncertainty weighed on the global economy, economic development in many countries has thus far remained more resilient than had been assumed. Inflation remained elevated in the US, while in the euro area it was close to target.

In its baseline scenario, the SNB anticipates that growth in the global economy will be moderate over the coming quarters. Inflation in the US is likely to remain elevated for some time. In the euro area, on the other hand, inflation is expected to stay close to target.

Uncertainty has decreased somewhat compared to the last monetary policy assessment. That said, the baseline scenario for the global economy is still subject to significant risks. For example, US tariffs and trade policy uncertainty could yet weigh more heavily on global economic momentum than observed thus far. It is also possible that trade barriers may be raised again. At the same time, however, it cannot be ruled out that the global economy will continue to develop better than expected in the coming quarters.

Swiss GDP contracted in the third quarter. The decline was due in particular to the pharmaceuticals industry. Value added there had risen strongly in the first quarter because deliveries to the US had been brought forward in anticipation of possible tariffs. There was a countermovement in the second quarter, which continued in the third quarter. Value added rose slightly in the other manufacturing industries and in services. Owing to this subdued economic development overall, unemployment has risen further in recent months.

The economic outlook for Switzerland has improved slightly due to the lower US tariffs and somewhat better development globally. For 2025 as a whole, the SNB expects GDP growth of just under 1.5%. For 2026, it expects growth of around 1%. In this environment, unemployment is likely to continue to rise somewhat.

The main risk to the economic outlook for Switzerland is the development of the global economy.

More detailed information on the monetary policy decision can be found in the introductory remarks by the Governing Board (available on the SNB website from 10 am on 11 December 2025).

{kind=link}

{kind=link}

{kind=link}